Where Tokenization Actually Completes the Equity Ecosystem

Every few months, “tokenized equities” gets rediscovered as the thing that ends Wall Street as we know it. Twenty-four-hour trading, fractional everything, the death of the intermediary. It is a great story. It is mostly wrong, and being precise about why matters, because there is a real opportunity underneath the noise.

This is a field map, not a forecast. The goal is to mark, end to end, where a shared ledger genuinely completes the equity ecosystem and where it does not, and to dispel the hype by being specific rather than breathless.

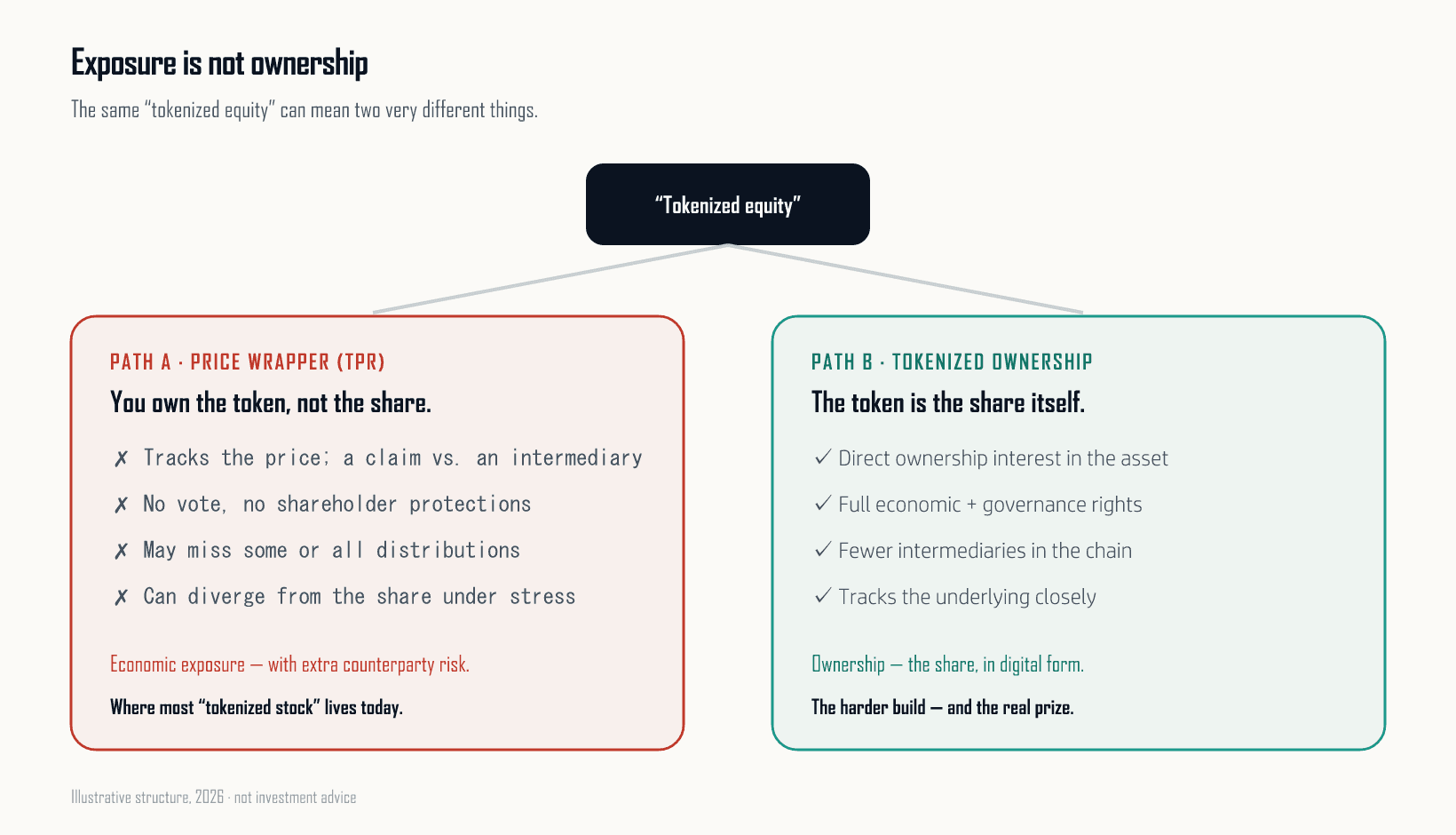

01Most “tokenized stock” isn’t a share

The hype collapses two very different things into one word. A token can give you the price behavior of a stock, or it can give you the stock. Today, most “tokenized equities” are the former: a wrapper that tracks the price while you hold a contractual claim against an intermediary, with no vote, no shareholder protections, and a price that can drift from the underlying. That is exposure. It is not ownership.

The difference shows up exactly when it matters: in your rights, your recourse, and how the thing behaves under stress.

BlackRock recently made the same distinction explicit in its own investor education (exposure versus ownership), which is a useful sign that the serious institutions are now drawing the line clearly. If you do not know which one you are holding, you do not know what you own.

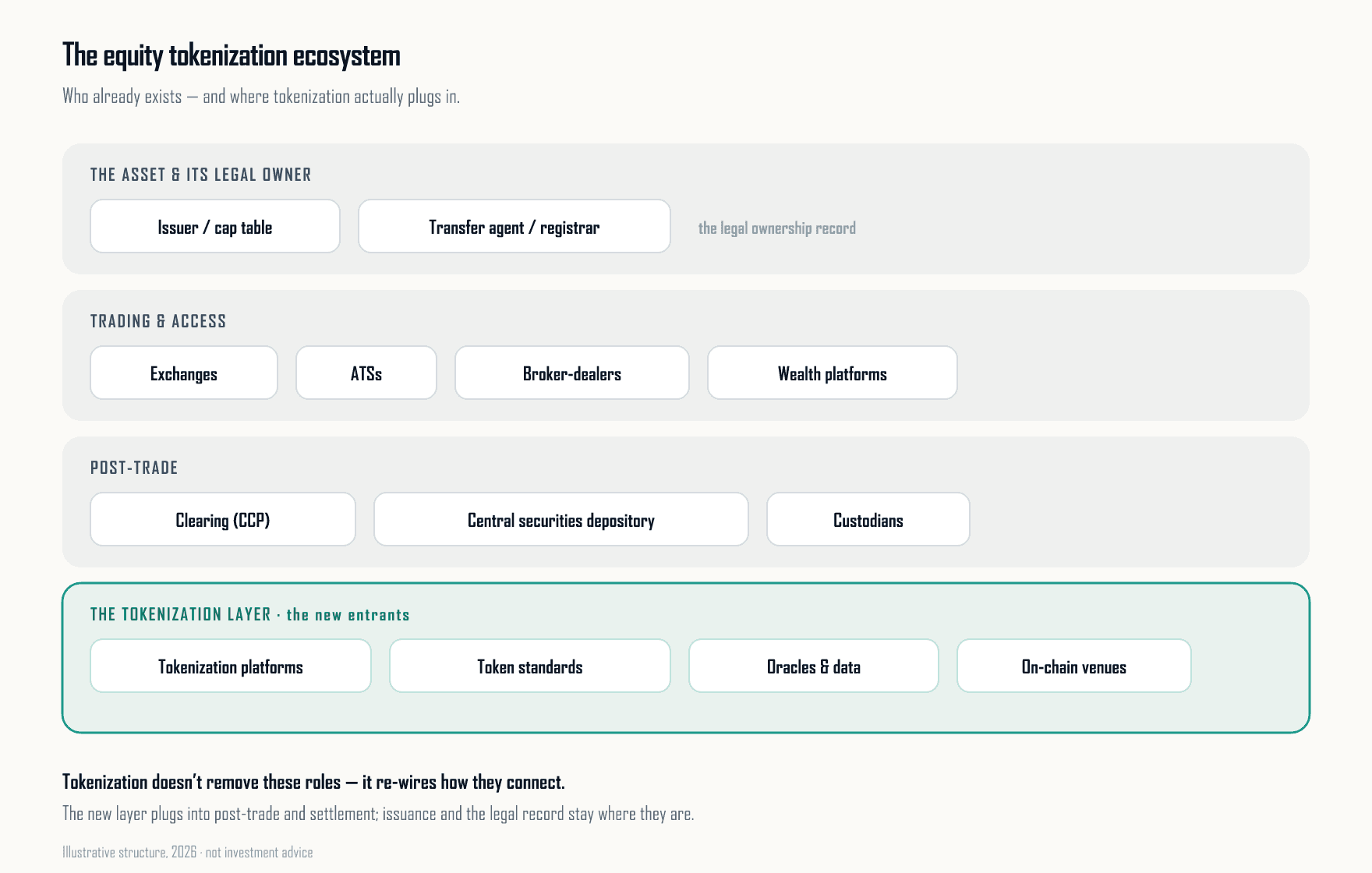

02The ecosystem doesn’t disappear

Equities are embedded in decades of legal and operational machinery: issuers and cap tables, transfer agents and registrars who hold the authoritative ownership record, exchanges and broker-dealers, clearing, the central securities depository, custodians. A token does not repeal corporate law or make the registrar vanish. Anyone selling “everything on-chain” is selling the wrapper and calling it the rails.

What the tokenization layer actually does is plug into that structure, most usefully at the post-trade and settlement end, and change how the pieces connect.

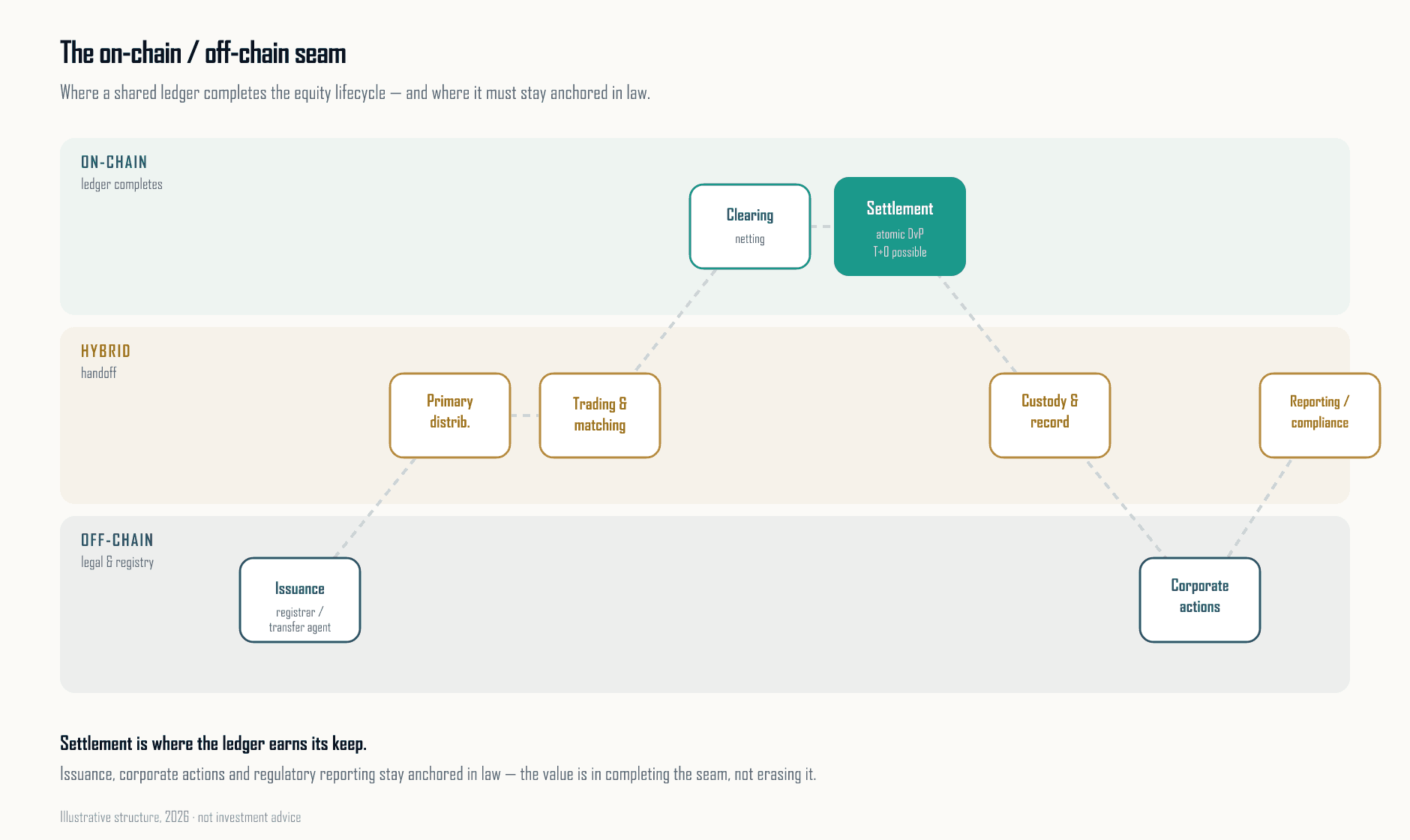

03Where on-chain completes it

This was never “on-chain versus off-chain.” It is a map. Walk the equity lifecycle end to end and ask, at each stage, whether a shared ledger genuinely improves it, whether it must stay anchored in the legal and registry world, or whether it is a handoff between the two.

Do that honestly and a pattern appears. Settlement is the primary target. Atomic delivery-versus-payment, deterministic finality, and collateral mobility are the outcomes the industry is working toward. SIX Digital Exchange (SDX) has operated tokenized securities settlement in a regulated environment since 2021. DTCC, Chainlink, and major financial institutions have tested DLT-based workflows for fund data, tokenization, and capital-markets interoperability; broad equity-market atomic DvP deployment remains an open problem rather than a solved one. Clearing is close behind. Issuance, corporate actions, and regulatory reporting stay anchored in law. Most of the lifecycle in between is a hybrid handoff.

The value isn’t in putting everything on-chain. It’s in completing the seam: optimizing the few stages a ledger truly improves, and leaving the rest where the law already works.

The seam map at the top of this piece is the whole argument in one picture: the dotted line is the lifecycle weaving between worlds, and the shape of that weave (not a slogan) is what an honest tokenization strategy has to respect.

What the map shows clearly: settlement and clearing are where a shared ledger creates measurable improvement in finality and risk. Issuance, corporate actions, and regulatory reporting stay anchored in legal and registry frameworks regardless of what rails sit underneath. The productive question is not whether a seam exists; it is where it belongs and how to design the handoffs precisely.

US equities moved to T+1 in May 2024. The industry question now is whether DvP-enabled on-chain settlement can go further — and what regulatory and operational alignment that requires. This illustrates the concept; broad deployment for equities is not yet in place.

The US moved to T+1 in May 2024, compressing the cycle while preserving its sequential structure. The next step, T+0 via atomic delivery-versus-payment, has been demonstrated in regulated pilots. The remaining work is standardization: settlement finality rules, custodian integration, and messaging interfaces that span on-chain and traditional counterparties.

04Settlement is not one thing

There is a trap hidden in the sentence “settlement is the primary target.” It treats settlement as a single thing with a single best answer: faster, atomic, instant. Walk into any wholesale trading operation and that assumption falls apart. Settlement has two dimensions that legacy rails force you to trade against each other: how much counterparty risk you carry, and how much capital you tie up.

Almost no one in institutional markets actually wants gross, trade-by-trade finality, and they never did. Netting exists precisely because institutions value capital and liquidity efficiency. In the US, the NSCC’s continuous net settlement compresses the obligations that actually have to move by roughly 98 percent before anything settles. Pure atomic settlement throws that away. It removes leg risk by forcing every leg to be pre-funded and delivered in full, in real time. That is a return to a pre-netting world, which is the irony buried in “24/7 instant settlement”: wholesale markets spent decades moving away from gross settlement on purpose.

The honest frame is not gross versus netted. It is a trilemma between three properties every market would like at once: counterparty-risk elimination (no leg risk), capital efficiency (netting), and intermediary minimization (no central risk-bearer). Today you can hold any two. Holding all three is the unsolved problem.

What a shared ledger actually changes is not “settlement becomes instant.” It is that a programmable ledger can decouple settlement cadence from settlement finality. Net over whatever window you choose, continuous, hourly, or end-of-day, and settle the net position atomically at the boundary. Atomicity stops meaning “every trade, immediately” and starts meaning “the net is final and indivisible.” The netting cycle becomes a parameter rather than a fixed property of the infrastructure.

The question is not how fast settlement can be. It is whether the cadence can be a dial, and who holds the risk while it turns.

That reframes the hard problem rather than removing it. Netting is inseparable from someone bearing the risk during the window. Compress the window to zero and you are back to atomic gross, capital cost and all. Keep the window, and you either fully collateralize it, which brings the capital cost back, or something novates and mutualizes it, at which point you have rebuilt the central counterparty, possibly in code, with all of its margin, default-management, and governance questions intact. Which of those the market chooses, asset class by asset class, is one of the defining design decisions of the next decade. And because that cadence has to be communicated between systems on both sides of the seam, it is also a standards problem.

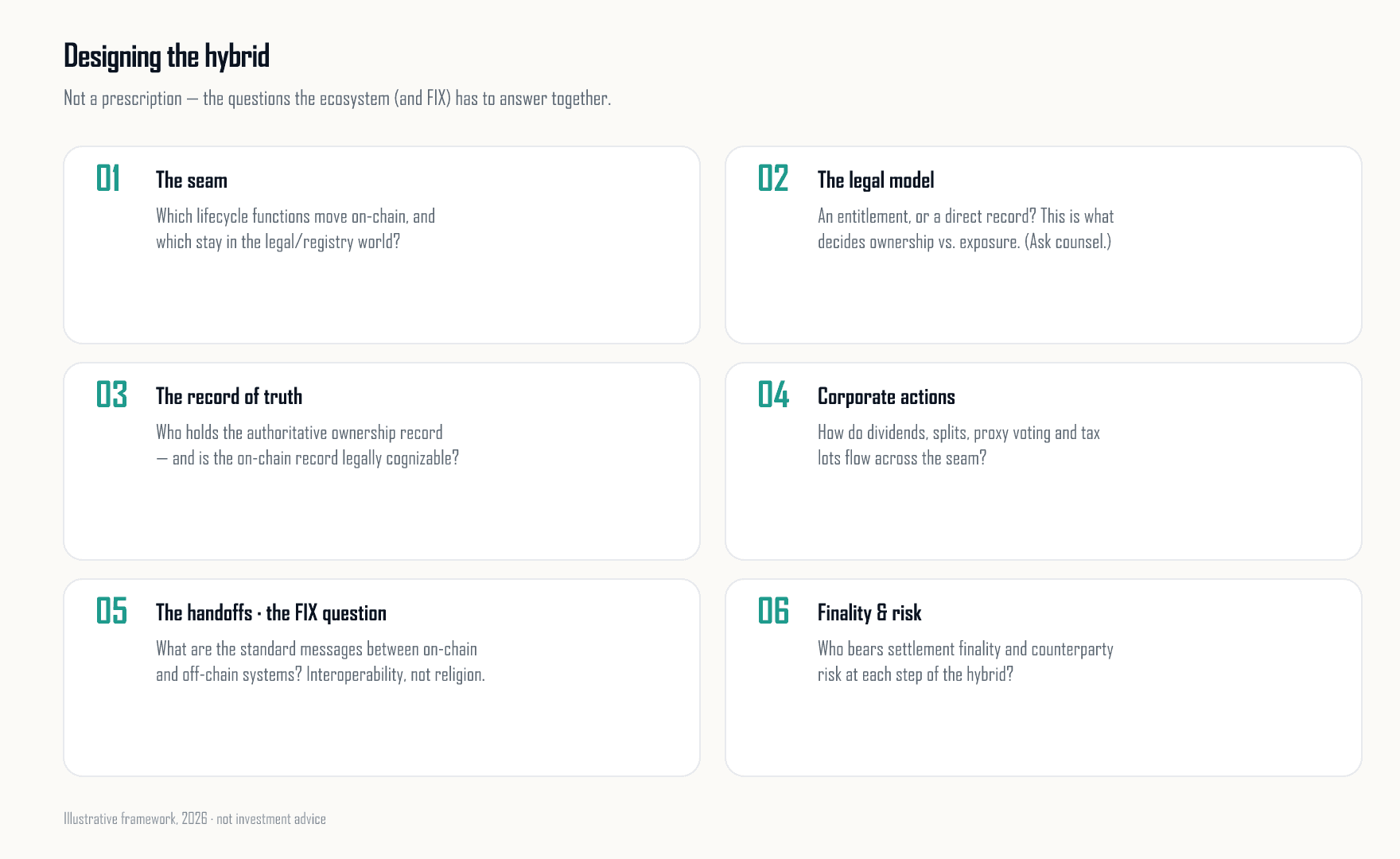

05Designing the hybrid is a standards problem

If the answer is a hybrid (and it is), the hard work is defining it precisely: which functions move, what the handoffs are, and who carries risk where. That is a standards and interoperability question, exactly the kind of work the FIX Trading Community is built to map. None of it is solved by shouting “on-chain” louder.

The shape of the hybrid will be decided by how the industry answers six core questions:

- Which functions actually move on-chain, and which remain anchored in existing legal and operational systems? Not all stages benefit equally: settlement and collateral mobility have the clearest on-chain improvement case, while issuance and regulatory reporting stay anchored in law regardless of the underlying rail.

- Is the tokenized claim a direct legal record of ownership, or merely an entitlement against an intermediary? (This single distinction determines whether you have true ownership or synthetic exposure.) The answer determines your rights in a stress event, your ability to vote, and whether corporate actions flow through automatically: it is a legal architecture question, not a marketing one.

- Who holds the authoritative record, and is the on-chain representation legally cognizable under current or evolving frameworks (e.g., UCC Article 12)? If the on-chain record mirrors an off-chain register rather than being the register, the settlement finality benefits of an on-chain system do not fully materialize.

- How do corporate actions, dividends, voting, and proxy mechanics flow across the on-chain / off-chain seam? These are the moments when the seam is most visible to end investors and where automation promises are hardest to deliver without a clear legal handoff protocol.

- What standard messages and data models will be used for handoffs between on-chain and off-chain systems? Without a common instruction format (the equivalent of FIX for traditional equity trades), each bilateral integration becomes a custom engineering project that does not scale across the market.

- Who bears settlement finality and counterparty risk at each step of the lifecycle? In a hybrid system, risk does not disappear; it migrates to the seam. Clarity on who holds risk at each handoff is what makes the system insurable and operationally sound.

The hype asks what we can put on-chain. The better question is what completes the system end to end, and how the two halves talk.

That is the map worth building together. The winners will not be the firms that tokenize the most things. The winners will be the firms that make tokenized ownership, settlement finality, corporate actions, and regulatory records work together without breaking the existing market contract.

References & Context

- iShares / BlackRock. “What Is Tokenization? Ownership vs. Exposure Explained.”

- DTCC / NSCC. Continuous Net Settlement (CNS): netting compresses the obligations that require settlement before anything moves.

- FIX Trading Community. Interoperability and messaging standards across the trade lifecycle.

- Uniform Law Commission. UCC Article 12 (Controllable Electronic Records) and the 2022 amendments.

Illustrative and educational only. Nothing here is investment, legal, or tax advice, or an offer or solicitation of any security. Public industry structures are referenced for context; consult qualified counsel before acting.